Europe's electricity demand is increasing. In the context of Europe's decarbonisation goals, this power will have to come from more variable Renewable Energy Sources. As European policymakers consider their options for invesments in new and more efficient grid infrastructure, they should take into account the benefits that PV is already producing and, more importantly, plan for the greater benefits it is capable of producing in the future.

Contributed by | EPIA

PV, A COMPETITIVE SOLUTION FOR THE DECARBONISATION OF EUROPE’S ENERGY SECTOR

The need to avoid irreversible climate change effects has led European Union (EU) countries to commit to reducing greenhouse gas emissions to 80-95% below 1990 levels by 2050. This implies an almost complete decarbonisation of Europe’s energy sector by the middle of the century due to the difficulty of cutting emissions in other economic sectors. Achieving this goal will have important consequences for the continent’s entire power system.

The Energy Roadmap 2050 presented by the European Commission (EC) in December 2011 and the October 2011 proposals for a renewed energy infrastructure policy offer a unique opportunity to rethink the evolution of the European energy mix and of its electricity grids as many investors consider their future plans in our continent.

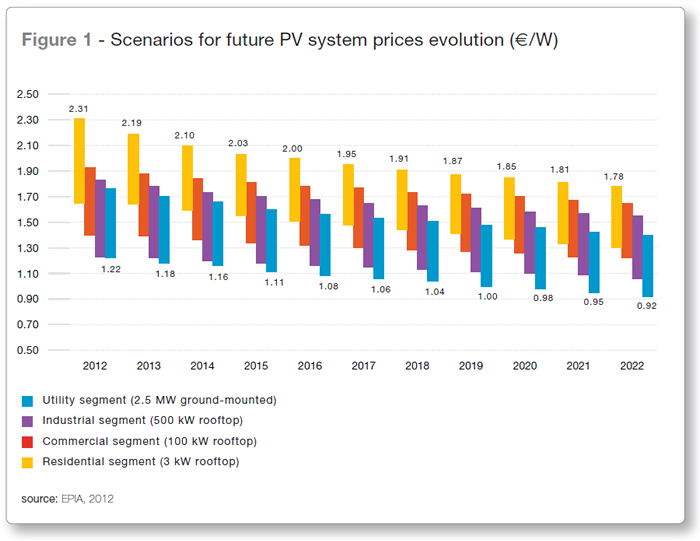

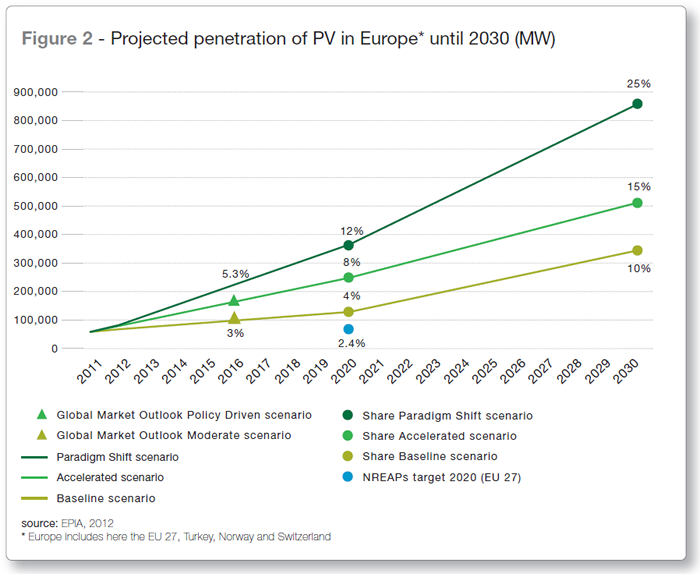

With a more diversified, variable and presumably electricity-intensive energy mix, the future European electricity system will have to be more interconnected, more flexible and more decentralised. The enhancements of the grids, both at distribution and transmission level, will accompany the complete transformation of the electricity sector. They should in particular integrate the rise of distributed generation, including solar photovoltaic (PV) electricity, which will play a key role in Europe’s electricity mix. Already in 2030, PV could cover up to 25% of electricity demand in Europe, thereby contributing to the decarbonisation of the electricity mix. This will be driven notably by its competitiveness trajectory and future system price evolution. As shown in Figure 1, PV system prices are expected to fall from up to 2.31 €/W in 2012 in the residential segment to as low as 1.30 €/W in 2022.

What does this mean concretely? The average price for a 3 kW household PV system was €20,000 in 2000 (excluding VAT). The average price of the same system is around €6,000 today in 2012 and is expected to go below €4,500 before the end of this decade.

The experience of the last decade shows that underestimating the full potential of PV leads to sub-optimal situations both from a capacity planning and a network operation point of view. Navigating through the transition towards a more sustainable energy future therefore requires tangible scenario-based forecasts.

This study prepared by the European Photovoltaic Industry Association (EPIA) aims to provide a holistic vision of how solar electricity will be integrated in the electricity system. It is based on new EPIA scenarios for the penetration of PV electricity in 2030 (Figure 2):

- The Baseline scenario envisages a business-as-usual case with 4% of EU electricity demand provided by PV in 2020 and 10% in 2030

- The Accelerated scenario, with PV meeting 8% of the demand in 2020, is based on current market trends, and targets 15% of the demand in 2030

- The Paradigm Shift scenario, based on the assumption that all barriers are lifted and that specific boundary conditions are met, foresees PV supplying up to 12% of EU electricity demand by 2020 and 25% in 2030

Did you know?

In Italy, PV already covers 5% of the electricity demand, and more than 10% of the peak demand. In Bavaria, a federal state in southern Germany, the PV installed capacity amounts to 600 W per inhabitant, or three panels per capita. In around 15 regions in the EU, PV covers on a yearly basis close to 10% of the electricity demand; in Extremadura, a region of Spain, this amounts to more than 18%.

These scenarios have been combined with corresponding wind penetration scenarios. From there, a detailed analysis of balancing needs has been conducted for all 27 EU Member States (based on intermediate scenarios) in order to better understand system operation challenges. At distribution level, the study analyses the main constraints associated with high shares of distributed generation. It also considers the effect that grid integration costs will have on the overall competitiveness of PV against other forms of electricity (which had previously been assessed in the EPIA study “Solar Photovoltaics Competing in the Energy Sector: On the road to competitiveness”, published in September 2011).

This work involved interviewing several network operators, both at transmission and distribution level, so as to identify best practices and build recommendations on the basis of real-world experience. The identified challenges have been answered with existing and potential future solutions, making the best use of PV systems capabilities, which are today vastly underestimated.

Highlighting the true potential of PV in EuropePV technology has shown an impressive resilience to harsh market conditions in 2011 and 2012. Thanks to its decentralised nature and its ability to lower prices due to its modularity, PV continues to outperform all growth forecasts. The 15% penetration scenario (Accelerated scenario) considered in this study represents a very realistic view of market development in Europe until 2030. It assumes roughly that the same absolute market conditions observed in Europe in 2011 will be sustained through the coming two decades. The “SET For 2020” study published by EPIA in 2009 estimated that PV could reach up to 12% of Europe’s electricity demand by 2020. This high-growth, Paradigm Shift scenario highlighted at that time the complex conditions required to reach such a goal. From 2008 to 2010, market growth in Europe reached levels compatible with such a high scenario. As a result, this Paradigm Shift scenario remains a possible future for PV until 2020. What makes this scenario useful is that the set of preconditions necessary to reach 12% are similar regardless of the date at which this level of penetration is reached. In particular, deploying grid integration solutions as described in this study will unleash the real potential of PV and make the 25% penetration scenario a realistic one. While this study “Connecting the Sun: Solar photovoltaics on the road to largescale integration” focuses on the 15% scenario in 2030, this level of penetration does not represent a final goal but rather a milestone towards higher levels. The question is: When can a 25% penetration be reached? In 2030 or later? |

PV, AN ACTIVE PART OF SYSTEM OPERATION IN EUROPE

The existing electricity system has been designed to connect large, centralised generating units to large consumers as well as to substations that deliver the power to smaller consumers and, finally, to households. At issue is whether the system can integrate a high number of distributed renewable generators, most of them PV and wind, without creating operational issues and affecting security of supply.

Until the massive penetration of Variable Renewable Energies (VRE), such as PV or wind, electricity generators were dispatchable, meaning their power output could be adjusted according to demand. They were controlled by the Transmission System Operator (TSO) on a permanent basis to meet demand and maintain the stability of the entire electricity system. However, VRE by nature are not dispatchable since they cannot always produce on demand. Moreover, actively managing power output of PV and other small generators requires the ability to control them, something not currently possible. Finally, while VRE can technically provide some flexibility, the need to develop a more sustainable energy mix requires maximising the injection of renewable electricity.

These concerns have been relatively minor with a low penetration of PV in the past; today and especially tomorrow they must be reconsidered as high levels of penetration are reached. This study examines the electricity system’s behaviour under normal as well as extreme conditions (peak electricity demand, minimum electricity demand) and reaches the following conclusions:

- Large-scale PV integration in the European grid is technically feasible with a high level of security of supply, even under the most extreme weather and load conditions. With the right measures in place, system reliability can be ensured

-

Solutions exist to address the challenges linked to the increased integration of PV and wind – their relative variability, their limited dispatchability, and the flexibility requirements they induce in the electricity system:

- Variability: While the production of a single PV unit can go up and down quickly under certain weather conditions, this has an insignificant effect on the overall electricity system. For this reason, PV should be considered as a variable source of electricity rather than an intermittent one. Indeed, the electricity output of a large number of PV systems is less variable than the output of a single PV system; the larger the number of systems and the area considered, the smaller the variability of the power generated by PV systems in that area (Figure 3). PV forecasting already provides a measure of reliability but is a new tool for PV operators as well as for TSOs and needs to be further developed; it will in any case be more precise if large numbers of PV systems are aggregated.

-

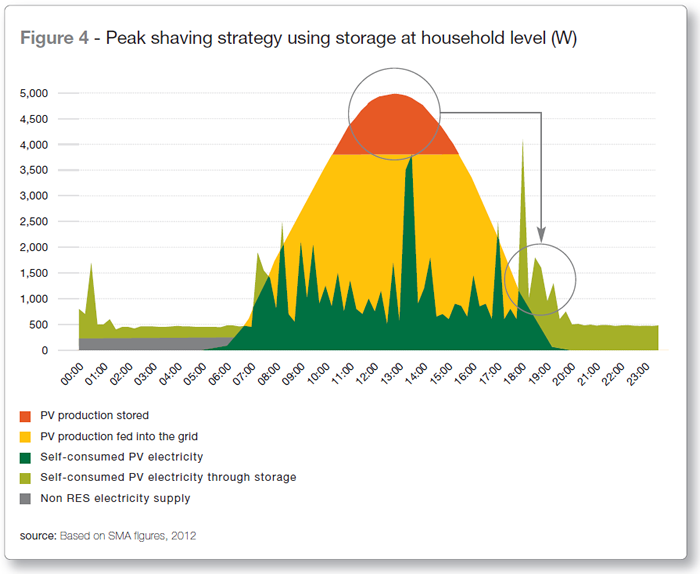

Dispatchability: PV peak production takes place around midday, which is the time when demand also reaches one of its daily peaks; this is an important strength of PV technology. In order to increase PV’s contribution to meeting the evening consumption peak, two solutions exist:

1) Shift part of PV electricity in-feed from the day to the evening with the help of storage facilities (Figure 4); or

2) Shift part of the evening consumption to earlier hours of the day with Demand Side Management (DSM) measures

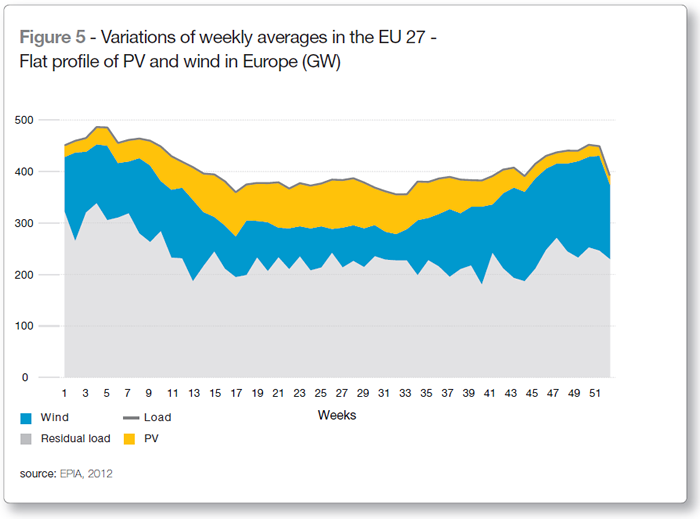

On a seasonal basis, the complementary output of PV and wind can reduce the need for back-up generation (Figure 5).

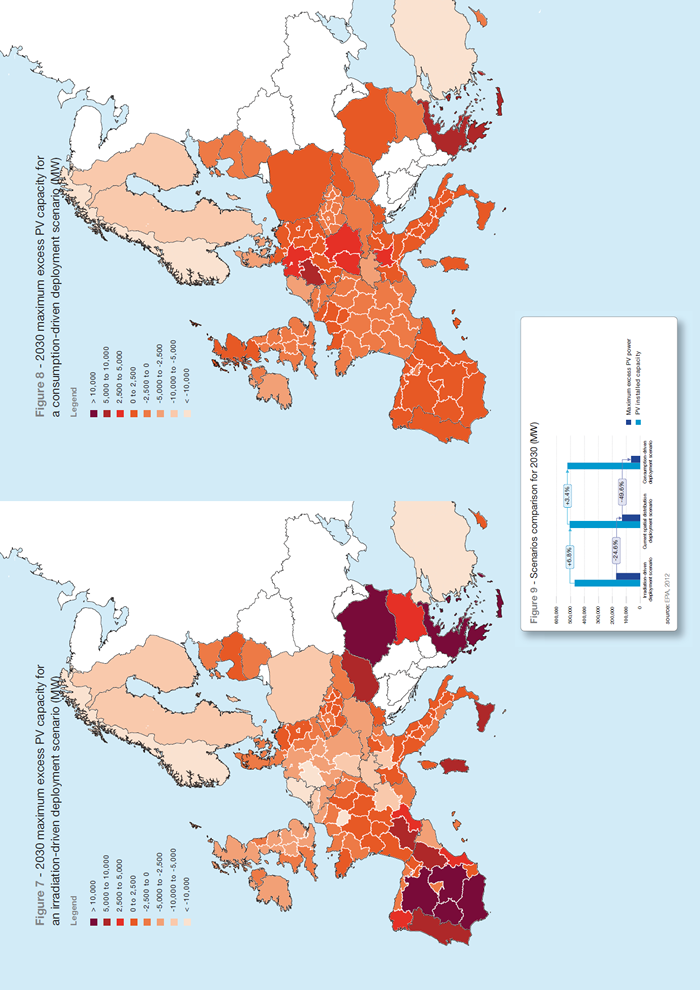

Finally, PV’s unique ability to produce electricity close to where it is consumed alleviates the need for additional massive investment in new transmission lines. As shown in the study, different PV deployment strategies can be implemented in order to reach a 15% PV penetration scenario. Favouring an EU irradiation-driven strategy would imply larger use of future transfer capacity. Focusing on dense consumption areas would require only 10% more installed PV capacity but would reduce by almost 75% the need to transfer the excess generation (Figures 7, 8, 9)

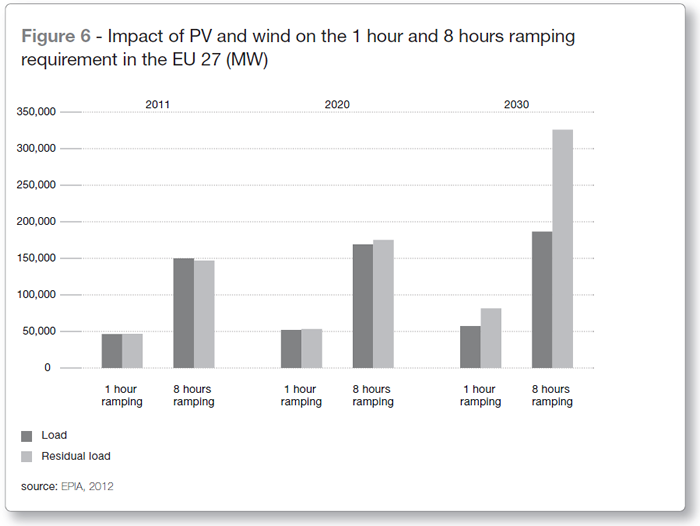

- Flexibility: To ensure adequate system flexibility in the future, i.e. the capacity to cover the constantly varying residual power needs, a proper mix of assets (interconnections, storage, DSM, flexible generation) should be used. The capacity of currently installed flexible sources to ramp up and down with fluctuations in demand will be sufficient until 2020 (Figure 6). To achieve the VRE penetration foreseen in 2030, additional flexibility will be required to reduce the periods during which part of the conventional power fleet will have to be operated in stand-by mode to respond quickly to any balancing needs. Since PV and wind production can be easily forecast, coordinated actions can be planned for these few hours

- To fully benefit from carbon-free electricity sources, storage and DSM solutions should be implemented soon and progressively, in order to avoid limiting the full exploitation of PV and wind electricity at the European level in 2030

Did you know?

Today’s best examples of DSM are found in the industrial and commercial segment, where normally there is an available communication infrastructure. Therefore using cheap electricity at nighttime is currently easier and more cost-efficient compared to DSM techniques at the household level.

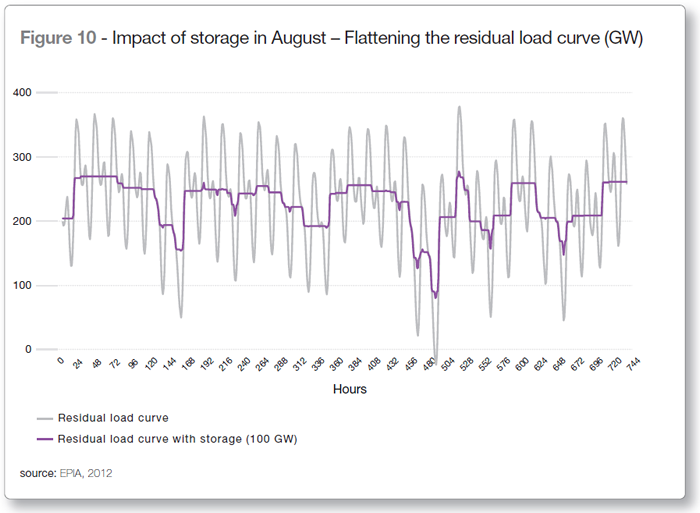

- Daily storage is well-suited for PV peak generation. This is because it is guaranteed that PV generation (in a large region) is available every day with a perfectly predictable peak that always occurs around midday. As the peak demand in Europe occurs in the evening hours the time shift between peak PV generation and the peak demand never exceeds eight hours. As shown in Figure 10, a 100 GW storage capacity can avoid excess generation and also reduce the peak demand, thus flattening the residual load curve in Europe. The former effect has a positive impact on the reduction of flexible stand-by capacity; the latter is a significant solution to excess generation (which wastes green energy) at EU level that might be seen on some days in 2030

PV AND THE FUTURE OF THE DISTRIBUTION NETWORK

As an extension of the transmission network, distribution grids must be managed to maintain the voltage level within specified limits and deliver a high quality of power.

Current distribution grids have been designed to transport the required power from the higher voltage level to the connected demand. Consumer electrical appliances are able to work only within certain margins for frequency and voltage. To avoid their degradation, system operators have to ensure that every consumer has access to secure and quality electricity.

The distribution network – which comprises Low Voltage (LV), Medium Voltage (MV) and in some countries High Voltage (HV) levels – has been designed to connect with small consumers: households, small and medium enterprises and small industrial sites. The rise of distributed generation, such as PV, in the distribution grid now means that electricity flows in two directions: from the transformer to the consumer, but also vice-versa.

After assessing the feasibility of integrating high amounts of variable renewable electricity at the distribution level by increasing the hosting capacity of the grids, this study finds that:

- Already today, several Distribution System Operators (DSOs) are managing significant penetrations of distributed generation in Europe; there are today no technical limits to large-scale PV integration. Large-scale PV integration depends on PV hosting capacity, which is limited by two factors: the maximum operating voltage (due to the voltage rise) and the maximum current loading (due to the overload of grid components)

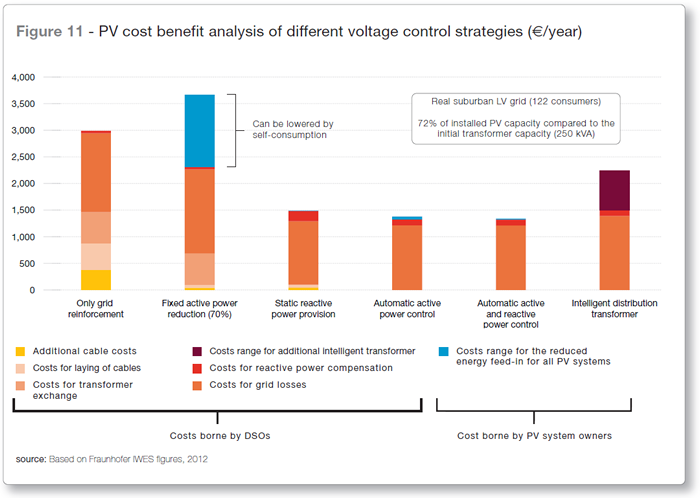

- Nevertheless, to avoid the need for costly interventions in the future, DSOs should implement “smart solutions” allowing for even more and smarter PV participation in system operation (Figure 11), including: grid monitoring, self-regulated or controlled distribution transformers and decentralised storage

- These solutions should build on a better assessment and simulation of the impact on the grid of a rising share of distributed generation that should be conducted on a regular basis

- PV can already provide significant grid support capabilities, including active power reduction, fault ride-through, and voltage support; these capabilities are currently vastly underrated. Some countries still consider that PV systems should behave as passively as possible. Only a few countries take into account the ability of inverters to address the impact of PV on the distribution grid. Moreover, it is often unclear what requirements PV inverters should meet. Enhanced dialogue between the PV industry and DSOs is therefore needed. The need to harmonise requirements is important to avoid product variance and instead favour a cost-effective PV deployment

- Curtailment should not be considered the silver-bullet solution for increasing the hosting capacity of the distribution grid, given that PV systems can also provide voltage support at virtually no cost

- Enabling a higher level of self-consumption will also reduce system congestion

- To reduce peak production and/or consumption, strategies will have to be implemented using DSM measures or storage at the household or local level. Standards for inverters and for communication infrastructure (including smart meters) will enhance PV system capabilities and ensure a cost-effective grid integration of PV

IMPACT OF GRID INTEGRATION ON PV COMPETITIVENESS

Until now, the PV market has been helped in its development by financial support schemes such as Feed-in Tariffs, but these will be progressively phased out. EPIA’s 2011 report, “Solar Photovoltaics Competing in the Energy Sector: On the road to competitiveness”, showed that competitiveness of PV is approaching quickly in many European markets. Since the publication of that study, production overcapacity on the PV market has driven prices down faster than expected, bringing some market segments in specific countries close to the first level of competitiveness already. But the question about the future remains: How will grid integration challenges affect PV competitiveness?

This new study explores the impact of potential additional costs – either directly linked to PV participation in grid operation or related to the necessary system evolution – and reaches the following conclusions:

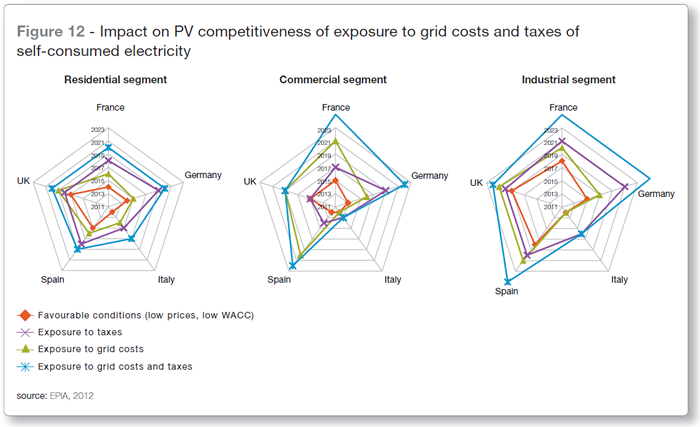

- The costs associated with increased PV participation in system operation will, depending on the measures involved, have an impact on PV competitiveness (Figure 12)

- The costs of widespread deployment of state-of-the-art capabilities in PV inverters will be negligible

- However, curtailment would have a considerable negative impact on the revenue stream of PV system owners, even when the cuts are limited; it should therefore be used only in extreme grid situations and after all other technically more efficient options have been executed

- If PV system owners are required to pay grid costs and taxes even when selfconsuming electricity, PV competitiveness will be delayed by a certain number of years depending on the market segment and on the country

Other smart solutions to enhance PV penetration have an impact on its competitiveness:

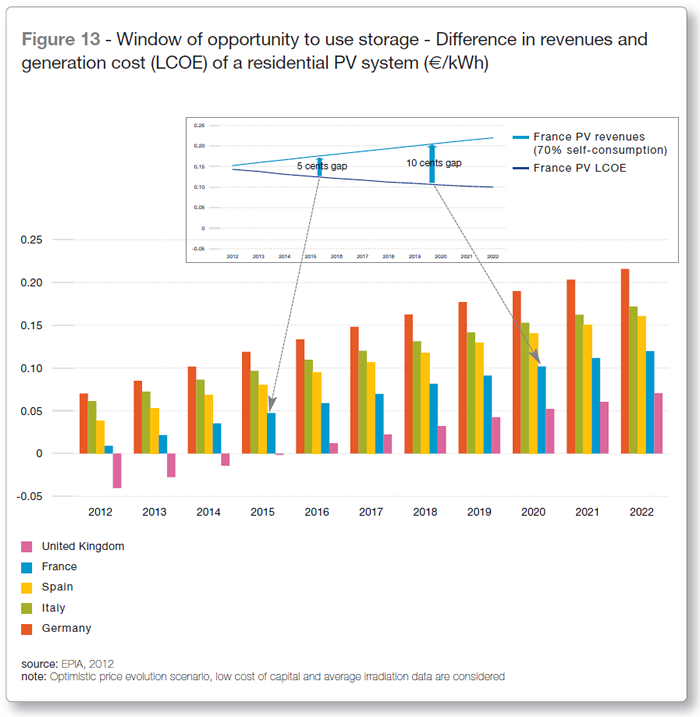

- On the one hand, the increasing competitiveness of PV systems will also allow more room to invest in storage. The combination of PV and storage will become more and more economically attractive as the electricity savings from storage will exceed the revenues from the electricity sold on the wholesale market (Figure 13, example of France)

- On the other hand, DSM measures would bring forward in time the competitiveness of PV. A combined PV-heat pump system today represents one of the best ways to optimise self-consumption and therefore increase the competitiveness of PV

POLICY RECOMMENDATIONS

There are virtually no technical limits to PV integration into the electricity system. But integrating large shares of distributed generation in the electricity system requires a series of complementary measures. Not all of them are of a technical nature. A lot has to be done also to ensure a closer collaboration among TSOs, DSOs, and conventional and renewable players in order to identify cost-optimal solutions. PV in itself will be one of these solutions, through the provision of grid services and, in some cases, contracted curtailment.

System operation will become more complex, since PV and wind together will exceed occasionally the absorption capacity of the network. To maintain system security, it will be crucial to fully exploit and develop system flexibility. Here again, PV will be part of the solution, in combination with storage and DSM.

As Europe plans investments in new energy infrastructure, these evolutions should form the pillars of an integrated approach in which modification of the electricity system and development of the infrastructure are seen together.

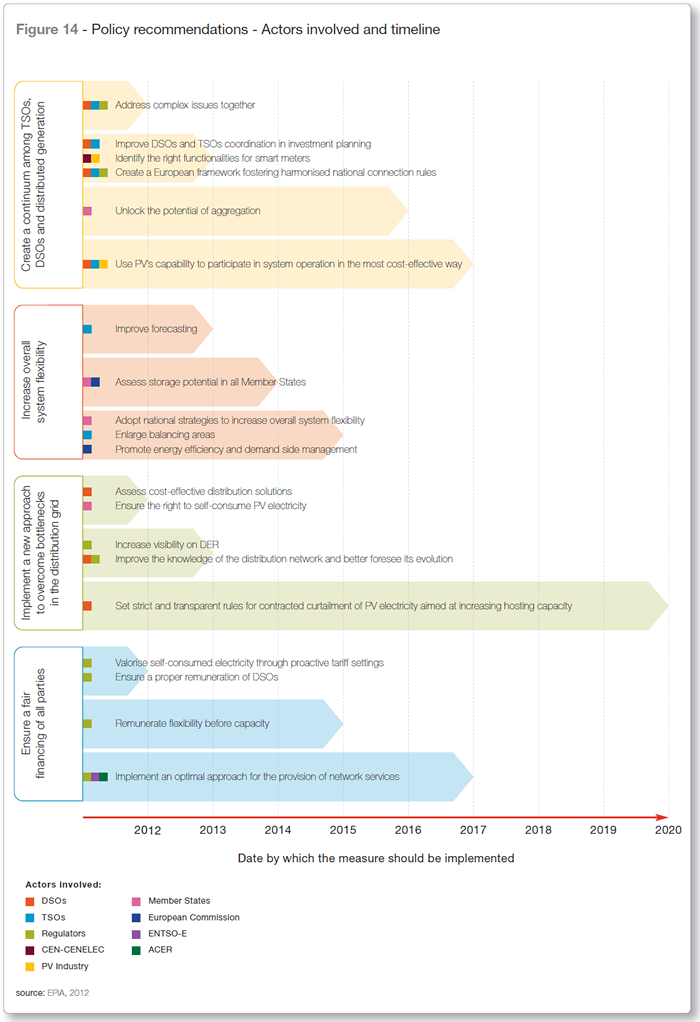

Such an approach requires several key policy goals:

Create a continuum among TSOs, DSOs and distributed generation

- Address complex issues together. The electricity sector and the PV industry will have to build up a constant dialogue to increase their mutual understanding

- Improve DSOs and TSOs coordination in investment planning. Currently, communication between DSOs and TSOs is not yet completely adequate

- Use PV’s capability to participate in system operation in a cost-effective way. PV generators should not bear responsibilities that could be borne by other generators at lower cost

- Create a European framework fostering harmonised national connection rules. Relevant European standards developed by European Standards Organisations should properly be taken into account in national regulation during grid codes revision processes

- Unlock the potential of aggregation. A regulatory framework at national level should be put in place Europe-wide, so as to allow new or existing actors to provide aggregation and valorisation of PV electricity and services

- Identify the right functionalities for smart meters. Two-way communication on active/reactive power input/off-take and remote control of power flows should be considered by European Standards Organisations as additional functionalities of smart meters. Future communication protocols should remain open and should be established at European level so as to ensure compatibility across the European Union

Increase overall system flexibility

- Adopt national strategies to increase overall system flexibility. Taking into account market and regulatory barriers, EU Member States should adopt by 2015 a roadmap identifying the best mix of measures to fully exploit their flexibility potential

- Assess storage potential in all Member States. National authorities should assess by 2014 the potential for storage deployment on their territory, considering optimal scale and technology

- Enlarge balancing areas. A real European vision of balancing should be developed so as to help integrate variable renewables in the power system

- Promote energy efficiency and demand side management. An appropriate regulatory framework for energy efficiency and DSM should be further promoted at European level

- Improve forecasting. PV forecasting methodologies should be implemented in the control routine of each TSO. There is still room to improve accuracy

Implement a new approach to overcome bottlenecks in the distribution grid

- Improve the knowledge of the distribution network and better foresee its evolution. To optimise their investment strategies, DSOs should constantly monitor and regularly run a prognosis exercise on the gradient of the increasing share of Distributed Energy Resource (DER) installed capacities in their operation area

- Assess cost-effective distribution solutions. Before making investments that allow for higher accommodation of decentralised electricity production, DSOs should undertake a cost-benefit analysis of all possible solutions, comparing grid extension and reinforcement with other available measures, including the exploitation of PV system capabilities

- Increase visibility on DER. Comprehensive information on PV installations should be reported to DSOs in a timely manner; such data should be aggregated and provided to the relevant TSO

- Ensure the right to self-consume PV electricity. By 2014 a proper regulatory framework allowing for self-consumption of PV-generated electricity should be in place in the EU Member States

- Set strict and transparent rules for curtailment of PV electricity aimed at increasing hosting capacity. In some limited cases, curtailment may be identified at distribution level to allow for a higher penetration of variable Renewable Energy Sources (RES) and to alleviate a temporary structural congestion issue. It should, however, be proposed only as an option in the framework of a contract between the DSO and the power generating unit owner, which should ensure a proper compensation of the power generating unit owner

Ensure a fair financing of all parties

- Implement an optimal approach for the provision of network services. PV will provide support to system operation if adequately remunerated; a balance should be struck between network codes and market-based mechanisms

- Valorise self-consumed electricity through proactive tariff settings. PV self-consumed electricity should not be exposed to the payment of grid costs and taxes

- Ensure a proper remuneration of DSOs. Tariffs and their design – as set by national regulators – should ensure a fair rate of return for DSOs

- Remunerate flexibility before capacity. Flexibility capabilities should be rewarded on the basis of a clear ranking among the various options

ON THE ROAD TO LARGE-SCALE GRID INTEGRATION

The increasing role played by variable RES, including PV, in Europe’s electricity system presents challenges for grid operators. However, in many ways, PV is already providing solutions – meeting a growing share of electricity demand at increasingly competitive cost without creating undue strain on the power system.

Even though it is not by nature dispatchable, PV electricity is decentralised and can be produced close to where it is consumed. Furthermore, it has a strong seasonal match with wind (since PV is able to meet more peak demand in summer, while wind is more productive in winter) and an average daily match (since PV produces during the day with a peak around midday, while wind produces more during less sunny hours); these two energy sources together can provide up to 45% of Europe’s electricity needs in 2030. When viewed together (and when considered from a Europe-wide perspective rather than a local or national one), they provide realistic solutions to the technical challenges involved in integrating this large share of renewable electricity. In any case, these solutions are achievable, especially when combined with tools to increase the flexibility of the electricity system – such as storage and demand side management.

Europe’s electricity demand is increasing. In the context of Europe’s decarbonisation goals, this power will have to come from more variable RES. As European policymakers consider their options for invesments in new and more efficient grid infrastructure, they should take into account the benefits that PV is already producing and, more importantly, plan for the greater benefits it is capable of producing in the future. In that way, PV can deliver on its promise as a major contributor to meeting Europe’s energy, environmental and economic goals for the coming decades.

The full report and the annexes can be downloaded from www.connectingthesun.eu.

References

“EU Energy Roadmap 2050”, European Commission, 2011

“Draft Regulation on Guidelines for trans-European Energy Infrastructure”, European Commission, 2011

“Draft Regulation Establishing the Connecting Europe Facility”, European Commission, 2011

“Harnessing Variable Renewables – A Guide to the Balancing Challenge”, International Energy Agency (IEA), 2011

“Solar Photovoltaics Competing in the Energy Sector: On the road to competitiveness”, EPIA, 2011

“SET For 2020“, EPIA, 2009

“Global Market Outlook for Photovoltaics until 2016”, EPIA, May 2012

“Pure Power”, European Wind Energy Association (EWEA), 2011

V. Wachenfeld, “Intelligent integration of decentralized storage systems in low voltage

networks”, SMA Solar Technology AG, June 2012

“Technology Compendium 3.4: PV Grid integration 4th edition”, SMA Solar Technology AG, May 2012

T. Stetz and al, "Improved Low Voltage Grid-Integration of Photovoltaic Systems in Germany”, Fraunhofer Institute for Wind Energy and Energy System Technology (IWES), 2012

Principal authors and analysts: Manoël Rekinger, Ioannis-Thomas Theologitis, Gaëtan Masson, Marie Latour, Daniele Biancardi, Alexandre Roesch, Giorgia Concas, Paolo Basso

Editor: Craig Winneker

Publication coordination: Benjamin Fontaine, Marie Latour

Contributions: This report was produced with analytical and technical support from 3E, and in particular Paul Kreutzkamp, Jan De Decker, Karel De Brabandere and Maximilien Croufe

Solar irradiation has been derived from the SolarGIS database:

http://solargis.info (©2012 GeoModel Solar)

Design: Onehemisphere, Sweden

Image: cover: © Allard1/Dreamstime

.png)

EPIA - the European Photovoltaic Industry Association - represents members active along the whole solar PV value chain: from silicon, cells and module production to systems development and PV electricity generation as well as marketing and sales. EPIA’s mission is to give its global membership a distinct and effective voice in the European market, especially in the EU.

The content & opinions in this article are the author’s and do not necessarily represent the views of AltEnergyMag

Comments (0)

This post does not have any comments. Be the first to leave a comment below.

Featured Product